eFX Apex

The Institutional-Grade Data Hub

- Plus: Discretionary Trades

- Edge: Sentiment Trades

- Alpha: Systematic Trades

- Apex: Full Big Data Stream

• USD net spec G10 long +$4.11bn to +$45.4bn in the Jul 15-21 IMM period; $IDX +0.3%

• Note- recent geopol climate hot, has lifted oil considerably boosting USD haven appeal

• EUR$ -0.21% in period; specs -28.7k contracts now -41.3k; ECB at 70% odds for Sept hike

• $JPY +0.57%; specs -29.5k contracts now -152.1k; USD firm awaiting BoJ hikes, intervention

• GBP$ -0.09%; specs +15.7k contracts now -55.6k; New UK PM stirs fleeting short unwind

• $CAD +0.35%; specs +1.8k contracts now -174.4k; soft CA inflation, hawkish Fed vibe lifts USD

• AUD$ +0.34%; specs -7k contracts now -37.7k; bottom-fishing likely ran into oil rise in current period

Majors w/IMM Performance Chart:

IMM Position Table as of 7-24:

(Paul.Spirgel is a Reuters market analyst. The views expressed are his own)

The dollar was mixed on Friday, trimming recent gains against some currencies but edging higher versus others as easing oil prices and lower Treasury yields prompted some pre-weekend profit-taking in a low-turnover session. Pakistan and Iran are exploring a path to renewed talks with the U.S. in a China-backed diplomatic initiative.

Weekend risks are heightened after U.S. President Donald Trump said earlier this week he is close to deciding on a "massive attack" against Iran. Trump said Friday that he does not believe China or Russia are involved in the Iran conflict, warning any involvement would be "very bad" for them. Trump criticized the EU's fines on Google, saying the U.S. would investigate what he called unfair targeting of American firms. ECB chief economist Philip Lane said the inflation shock remains moderate, requiring only limited policy action, with inflation expected to return to 2% within about a year.

The dollar index retreated from its 20-day upper Bollinger, suggesting a low-turnover, range-trading environment remains intact even as Middle East tensions build. EUR/USD remained biased lower, with an inverted hammer and position below 1.14 and its 21-day moving average of 1.1414 reinforcing a bearish outlook despite intermittent USD softness. GBP/USD stayed pressured below its 21-day moving average and near recent lows around 1.3300, with a broadly balanced Fed-BoE rate outlook and lingering geopolitical uncertainty limiting its upside. AUD/USD rose and remains biased higher, supported by a softer USD and strong commodity prices, with the pair consolidating gains above its 10-, 21- and 200-DMAs beneath the 0.70 level. USD/JPY remains constructive above 163 and a rising 21-DMA, though option barriers, intervention risks and geopolitical uncertainty may keep gains choppy, leaving the pair vulnerable to a pullback.

Treasury yields were down 1 to 3 basis points as the curve steepened. The 2s-10s curve was up marginally at +35.1bp.

The S&P 500 was flat as tech weakness was offset by other sectors.

WTI oil fell over 3% on profit-taking and the report of a fresh U.S.-Iran peace initiative.

Gold rose 0.20% while copper edged up 0.15% Heading toward the close: EUR/USD -0.07%, USD/JPY -0.01%, GBP/USD +0.09%, AUD/USD +0.20%, DXY +0.02%, EUR/JPY -0.08%, GBP/JPY +0.06%, AUD/JPY +0.18%.(Editing by Burton Frierson Robert Fullem is a Reuters market analyst. The views expressed are his own)

• NY opened near 0.6990 after 0.6966 traded overnight, the pair neared 0.6975 early

• Buyers emerged as USD, US yields , USD/CNH moved downward

• Gold, silver, copper & silver rallies added weight on the USD & buoyed AUD/USD

• 0.7001 traded but some gains eroded, the pair neared 0.6985 late, was up +0.24%

• Erosion of some gains for stocks, gold & silver helped AUD/USD slip from its high

• Techs lean bullish, pair held above 10- & 21-DMAs & is consolidating recent gains

• Rising monthly RSI and hold above the 200-DMA reinforce

bullish signals

audusd

(Christopher Romano is a Reuters market analyst. The views

expressed are his own)

Morgan Stanley Research maintains a neutral bias on the USD Index (DXY) in the near-term.

"We remain neutral on the DXY overall, but we see risks as decidedly skewed to the downside after two slower-than expected price prints in June: CPI and PPI," MS notes.

"The slowdown in US price pressures represents a downside risk to the ~29bp of Fed hikes priced through December 2026 (and therefore to the USD), since by September we expect broad disinflationary pressures to be increasingly evident in the incoming data – notwithstanding any potential energy price effects from geopolitical turbulence," MS adds.

AUD/USD is currently navigating a mix of short-term bullish signals and longer-term bearish risks. After giving back most of Friday's gains, the pair slipped back below the 10-day moving average, though shorter-term technicals still point to upside potential. Since the start of July, AUD/USD has been consolidating its recent rally, with a bull flag continuation pattern taking shape on the daily charts. If this pattern is completed, it could propel the pair toward the 0.7150–0.7200 zone.

However, this bullish scenario is closely tied to next week's Federal Reserve meeting—if the Fed holds rates steady or adopts a less hawkish tone than markets currently anticipate, the flag pattern may complete, allowing the rally from the June 29 low to resume.

Even if AUD/USD reaches the 0.7150–0.7200 target, bulls would face a critical test, as that zone represents significant resistance. Should the rally stall and then consolidate or retreat from that level, it could mark the formation of the right shoulder in a much larger head and shoulders topping pattern. Given the scale involved, this would be an unusually large pattern.

Should this major topping formation complete with a break of

the neckline, it would signal the potential for a substantial

decline—potentially pulling AUD/USD all the way down toward its

November 2025 monthly low.

audusd

(Christopher Romano is a Reuters market analyst. The views

expressed are his own)

Bank of America Global Research discusses EUR/USD technical outlook and sees a scope for an extended downside towards 1.1240 in the near-term.

Post ECB and US jobless claims on July 23, the euro fell and broke below trend line support. This implies a downtrend continuation pattern has formed.

Provided the downtrend continues, we can expect euro to retest the YTD low of 1.1325, the 1.13 figure and possibly the Fibonacci retracement at 1.1240," BofA notes.

We remain in favour of this short-term setup while euro remains below the high on July 23, which was 1.1436," BofA adds.

Sterling's recent struggles could persist as escalating tensions in the Strait of Hormuz and new US tariffs introduce significant headwinds for the global economy and, by extension, the UK. The widening conflict in a key oil shipping lane, coupled with President Donald Trump's fresh tariffs against trade partners signals a potential for sustained upward pressure on oil prices and disruptions to international trade. Rising gilt yields are also increasing market scrutiny over UK government financing, weighing on the pound. Although Prime Minister Andy Burnham has pledged fiscal responsibility and hinted at a new economic model, international investors are exercising caution, awaiting clearer details. Considering these intertwined geopolitical and domestic risks, the near-term outlook for sterling appears biased to the downside. Heightened geopolitical tensions, elevated oil prices, and an uncertain fiscal landscape in the UK advocate for a cautious approach to the currency.

Technically, GBP/USD currently finds support at 1.3299,

Thursday's low and the 61.8% Fibonacci retracement of

1.3140-1.3556, with further support at 1.3276, the July 2nd

daily low. To reverse the bearish sentiment, bulls would need to

push the pair above the 200-day moving average at 1.3399 and

clear the daily cloud top at 1.3411.

GBP$ Chart:

(Paul Spirgel is a Reuters market analyst. The views expressed

are his own)

Goldman Sachs Research previews next week's July BoJ meeting.

"The Japanese economy is recovering moderately in line with the BOJ's outlook. Although price trends are currently somewhat weak, we expect rising upstream costs to spill over to consumer prices going forward. Under these circumstances, in its July Outlook Report, we believe the BOJ is likely to maintain its broad scenario that the economy will continue to grow moderately albeit at a decelerated rate, and that CPI inflation will increase due to higher crude oil prices, but will subsequently decline as the impact of higher crude oil prices wanes," GS notes.

"However, with crude oil prices lower than when the April Outlook Report was published, we expect the BOJ to raise its growth forecasts and lower its price forecasts slightly in the July Outlook Report. We believe the BOJ will maintain the status quo at the July meeting, and continue to expect the next rate hike in January next year," GS adds.

ANZ Research previews next week's BoJ meeting and the scope for MoF intervention.

"While a hold is largely expected at next week’s BoJ meeting, the focus will be on the press conference and its updated forecasts which, in combination, may shape market pricing. An upward revision to FY26–27 inflation, would reinforce expectations of further tightening. A downgrade to growth on trade uncertainty would push in the opposite direction. Japan’s trade deficit widened this week as JPY weakness inflated the import bill. Import values rose 25% y/y in June, outpacing a 19% rise in exports. For now, the terms-of-trade drag points to softer net exports, near-term growth risks and continued pressure on the JPY," ANZ notes.

"Bottom line, the absence of intervention over the long weekend in Japan last week leaves the market with little reason not to test levels closer to 165 in USD/JPY. A sustained JPY turn would require more than verbal pushback; it would need at least a clear hawkish BoJ signal and more importantly a weaker USD," ANZ adds.

• EUR/USD hit 1.1376 overnight, buyers emerged and the pair turned positive

• 1.1401 traded in Europe, NY opened near 1.1385, pair was up +0.08%

• Lower USD, US yields , USD/CNH helped drive EUR/USD's gains

• Oil's drop & rallies in gold, silver, equities added buoyancy to EUR/USD

• Despite the gains technical signals still highlight downside risks

• EUR/UDS remains below the 10- & 21-DMAs and trend line off May 11 high

• Monthly inverted hammer candle, falling monthly RSI add to bear signals

• US July S&P Global PMI, June new housing sales are risks

in NY's morning

eurusd

(Christopher Romano is a Reuters market analyst. The views

expressed are his own)

• AUD/USD hit 0.6966 overnight, buyers emerged and the pair then turn positive

• Broad USD selling, soft US yields , USD/CNH drop buoyed the pair

• Rallies for gold, silver, copper and equities contributed to aiding the pair's lift

• 0.6995 traded in Europe's morning, the pair was up +0.36% in early NY action

• AUD/USD remains above the 10-, 21- & 200-DMAs which gives bulls comfort

• Ongoing consolidation & rising RSIs also comfort AUD/USD bulls

• US July S&P Global PMIs, June new home sales are data

risks in NY

audusd

(Christopher Romano is a Reuters market analyst. The views

expressed are his own)

• Cable tracking for its worst week in a month, off around 0.9%

• UK PMIs beat expectations, but price action muted with limited follow-through

• BoE survey further leans against need to tighten policy

• Modest support emerging around 1.3300, though rebounds remain shallow and unconvincing

• Elevated oil backdrop continues to weigh on GBP via terms-of-trade channel

• Break below 1.3300 opens a move toward 1.3250 as next downside target

• Resistance remains firm into 1.3390–1.3400 zone, capping

topside attempts

GBPUSD daily chart

Justin McQueen is a Reuters market analyst. (The views expressed

are his own).

((Email: ))

• EUR/USD slipped from the familiar 1.1400s to 1.1364 Thursday, before settling into a 1.1375-1.1400 range Friday

• Post Fed and 1-year low at 1.1325 and 1.1300 option barriers are key to deeper declines toward 1.1100

• 1.1104 is 50% Fibo retrace of 2025-2026 rally from 1.0125-1.2084, 38.2% is 1.1336

• FX options on alert for next week's Fed with USD calls in demand - they would benefit from lower EUR/USD

• Option risk reversals maintain a higher premium for downside over upside strikes, too

• However, option implied volatility retreats from Thursdays

highs and remains close to 2026 lows - no panic yet

EUR/USD daily chart (EBS)

EUR/USD 25 delta risk reversals

(Richard Pace is a Reuters market analyst. The views expressed

are his own)

• FX option traders said to have taken profits on upside bets, but some are reinvesting for more USD/JPY gains

• If 164.00 barriers are breached - short gamma positioning could fuel a further rise and topside options would benefit

• However, downside strike option demand outweighs that for topside and their premiums are significantly higher, too

• 1-month 25 delta risk reversals are 1.5 vol premium for JPY calls over puts - USD/JPY downside over upside strikes

• JPY calls would benefit from a spot setback and increased volatility - certainly one driven by FX intervention

• Japanese displeasure with USD/JPY gains is no secret, so the higher it goes, the more nervous the market becomes

• Related comment - War risk fuels Fed option bets

USD/JPY 25 delta risk reversals

(Richard Pace is a Reuters market analyst. The views expressed

are his own)

• Yen weakness persists despite intervention worries and the narrowing US-Japan rate gap

• USD/JPY rose to a new multi-decade high of 163.99, on Thursday

• Fin Min Katayama: Japan ready to take decisive action on forex

• US warns against excessive yen volatility, calls for BOJ rate hikes

• There are good offers ahead of 164.00, some likely option barrier defence

• Stops above 164.00 are large, however, speculators are eyeing massive barriers at 165.00

• USD/JPY has seen a 163.73-95, on Friday, according to EBS

data

Daily Chart

(Martin Miller is a Reuters market analyst. The views expressed

are his own)

• Oil has climbed back above $100 a barrel as Mid-East conflict escalation reignites inflation concerns

• Risk aversion lifts the USD and implied volatility, but gains in the latter appear tepid given the risks to FX

• That's because there is still a lack of actual/realised volatility upon which FX options thrive

• Benchmark 1-month EUR/USD implied volatility is 5.25, not much above recent and 2026 lows at 4.9

• However - 1-month daily realised volatility - often used as a fair value measure - is just 3.85

• In short - If EUR/USD spot repeats last month's performance - implied vol holders would lose money

• Related - FX options wrap - Oil, yields and Fed reignite

FX volatility risk

EURUSD FX implied vs realised vol

(Richard Pace is a Reuters market analyst. The views expressed

are his own)

• USD/JPY continues to hold relatively bid, Asia 163.73-95 EBS

• Holding below 163.99 high yesterday, 164.00

• 164.00 a point of contention, good offers, maybe on option barrier defence

• Stops above large however and specs eyeing more massive barriers at 165.00

• Fresh threats of FX intervention from FinMin Katayama but taken in stride

• That said, govt position on weak yen-inflation shifting?

• US Treasury also spoke out against yen volatility, for BOJ "normalisation"

• Govt coming round to need for FX action, BOJ hike?

• Tokyo still sees BOJ July hold but some say meeting "live"

• Total $2.4 bln in vanilla option expiries between 163.00-75 supportive

• $783 mln up at 164.00 strike too

• EUR/JPY to 186.65 EBS yesterday, best since 187.55 April 30, Asia 186.39-51

• Support from 186.32 hourly Ichi tenkan, kijun 186.26, cloud 185.76-89

• E652 mln in option expiries at 187.00 to help cap cross

• CHF/JPY sideways, Asia 200.33-75, CHF543 mln option expiries at 199 today

• GBP/JPY also sideways, 217.79-218.31, in recent higher range, 219.60 July 15

• AUD/JPY remained buoyant, 114.02-32, eyeing 114.91 high June 2, 115 test?

• Support seen from 114.03-16 hourly Ichimoku cloud, ascending 100-HMA 114.02

• NZD/JPY off 95.42 high Tuesday but holding own, Asia today 94.39-76

• Holding under ascending 200-HMA at 94.72, 94.90-95.06 hourly Ichimoku cloud

• Related comment , also , on MOF-speak

• On flows , Japan data , for more click on [FXBUZ]

USD/JPY hourly:

AUD/JPY hourly:

NZD/JPY hourly:

(Haruya Ida is a Reuters market analyst. The views expressed are his own)

• Shares of AGTech Holdings jump 7.6% to HK$0.71, on track for the biggest one-day pct gain since June 29

• Stock of Alibaba-backed electronic payment services provider snaps five striaght sessions of decline

• AGTech said on Thursday that its unit inked a technical service agreement with Hong Kong Gold Exchange (HKGX) to develop an electronic trading, clearing and settlement platform

• The fintech firm said all existing bullion trading, clearing, settlement and related electronic activities of HKGX are expected to migrate to the new platform after completion

• Hong Kong shares of Alibaba slip 4.2%

• YTD, AGTech stock up 248.3%, while Hang Seng TECH Index

down 15.8%

(Reporting by Donny Kwok)

• USD/CNY subdued, last 6.7742 from Thurs close 6.7777; SSEC -0.7%

• Capped by Ichimoku cloud 6.7785, also 21 and 55 DMA around 6.7830

• PBOC fix rises modestly to 6.7939 from Thursday's 41-mth low of 6.7906

• Damping decreased, as expected, to around +170 pips from +200

• USD/AXJ broadly subsiding as USD/JPY recedes away from 164.00

• Japan FM repeats warning on potential JPY intervention

CNY

(Ewen Chew is a Reuters market analyst. The views expressed are

his own.)

• Australian gold stocks fall as much as 3.9%, while the broader benchmark is down 0.5%

• Sub-index logs biggest intraday pct drop since July 17, but on track for a 1.7% rise for the week

• Gold prices dropped 2% overnight as escalating tensions in the Middle East sent oil prices surging and intensified inflation concerns [GOL/]

• Index leaders Northern Star Resources and Evolution Mining fall as much as 3.2% and 2.8%, respectively

• YTD, AXGD down 18.9%, including the day's moves,

underperforming a 0.9% rise in the AXJO

(Reporting by Nikita Maria Jino in Bengaluru)

• Yesterday saw USD/JPY leg up to 163.99 EBS, a tick shy of 164.00

• Market off since on inability to break above, offers up top, on options?

• Talk of some option barriers, Japan exporter offers likely in mix too

• USD/JPY 163.81-91 so far in Asia, specs likely looking for break above

• Stops likely on 164.00 break, massive option barriers at 165.00 in view now

• Japan's MOF conspicuous in its absence in ordering FX intervention

• Growing feeling among many in market MOF may not intervene at all

• Difficult to act with USD broadly strong, Middle East among factors

• Recently wider JGB-US Tsy rate differentials too, in 2s @281, 10s @189 bps

• US yields up on growing expectations of a more hawkish Fed

• Technically, support from flat hourly Ichimoku kijun at 163.49

• Seems equilibrium of sorts on 163 for now pending maybe fresh breaks up

• Option expiries today include 163.00-75 total $2.4 bln, 164.00 $783 mln

• Related comments , , ,

• And , also , on US Tsy stance on FX

• US markets , , ,

• On Fed , , US claims

USD/JPY:

USD/JPY hourly:

(Haruya Ida is a Reuters market analyst. The views expressed are his own)

• AUD/USD opens 0.45% lower after trading in a 0.69625-0.7021 range on Thu

• Undermined by risk aversion, U.S.-Iran tensions, surging oil prices

• Wall Street declines on AI spending worries, Brent futures settle over $100

• U.S. 10-yr yield jumps to 18-mth high on inflation concerns, Fed rate bets

• AUD drop limited by jump in AU jobs data Thu as RBA rate hike bets build

• Support at 0.6960-65 under threat, more support at 0.6945-50, 0.6920-25

• Resistance 0.6995-0.7000, stronger at 0.7020-25; Australia Q2 CPI Wed key

AUD:

(Krishna Kumar is a Reuters market analyst. The views expressed are his own.)

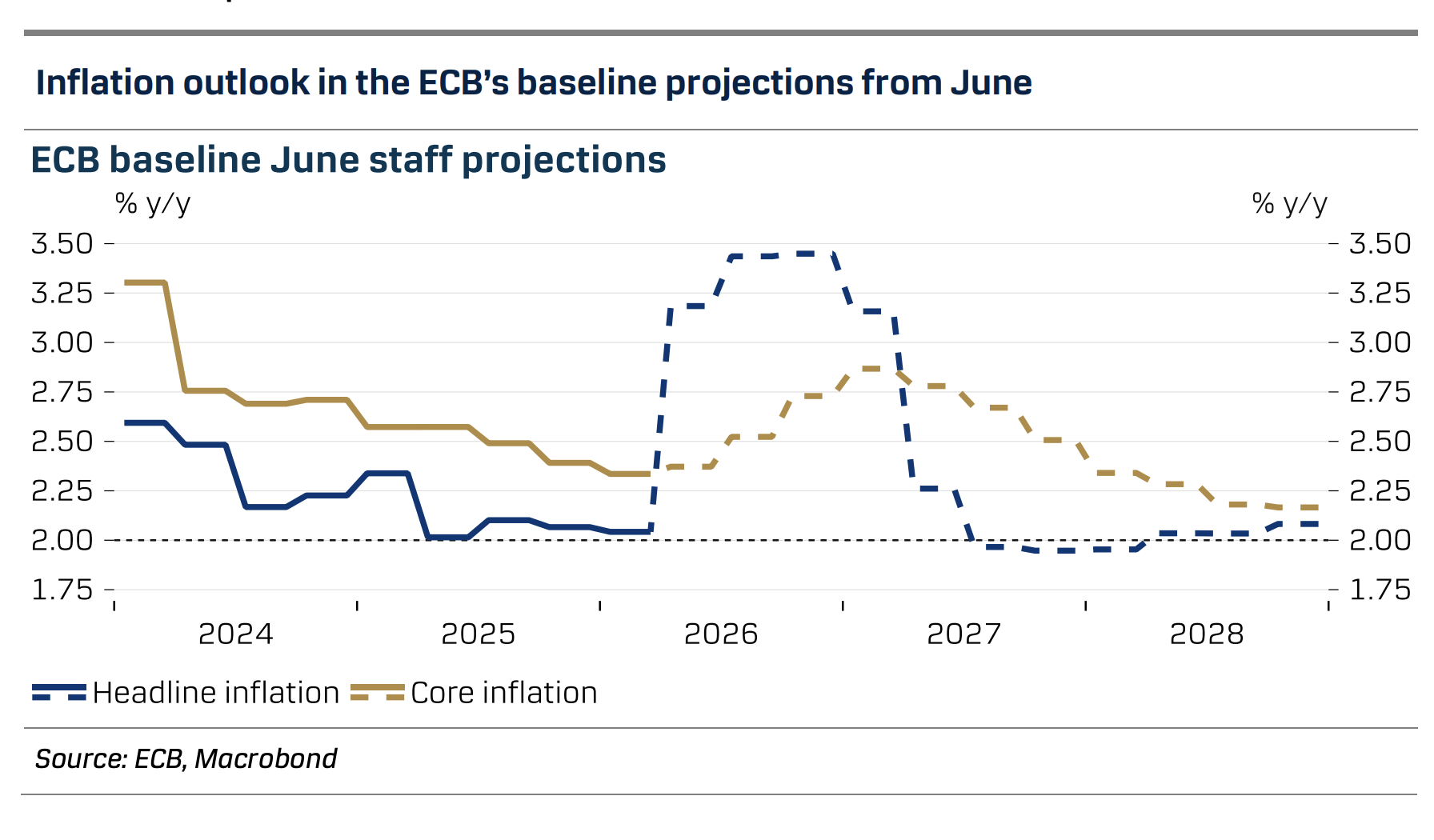

Danske Research reviews today's July ECB meeting.

"The ECB kept policy rates unchanged at the July meeting, with the deposit rate at 2.25%, in line with consensus and market pricing.

Lagarde kept full optionality on the future policy rate path, without precommitting. There was no market reaction to the meeting," Danske notes.

"We expect a final 25bp hike in September, bringing the deposit rate to 2.50%," Danske adds.

The euro slid after the European Central Bank left its policy rate unchanged as soaring oil prices amid escalating Middle East tensions and a selloff in technology shares fueled haven buying of the dollar. First-time U.S. jobless claims unexpectedly fell last week to their lowest level since the 1960s, signaling continued labor market resilience ahead of next week's Fed meeting. U.S. President Donald Trump said he is seriously considering renewed major combat operations against Iran and would hold Tehran responsible for any attacks by Yemen's Houthis. Trump also said a civil nuclear deal between the U.S. and Saudi Arabia is conditional on Riyadh joining the Abraham Accords normalizing relations with Israel. Yemen's Houthis said earlier on Thursday that they had carried out a military operation targeting two Saudi oil tankers. Additionally, Iran's Revolutionary Guards warned that the southern Strait of Hormuz shipping route has been mined. The European Central Bank, after leaving rates unchanged, kept the door open to a September hike as Middle East tensions cloud the energy outlook. ECB President Christine Lagarde said policymakers may discuss raising banks' minimum reserve requirements. Tech shares were pressured after Alphabet's first-ever cash burn and prospect of greater AI scrutiny after OpenAI's rogue incident. DXY surged to a three-week high, reaching its 101.54 upper Bollinger amid model-driven FX and fixed-income buying before trimming gains as tech shares retreated.

Option demand for dollar upside has risen, pushing one-month risk reversals to a 0.28% premium for the greenback, while the one-year tenor is approaching the 0.48% YTD high recorded in late June. EUR/USD remained under pressure below 1.14 as broad USD strength, rising yields, lower gold and a falling RSI suggest further downside toward its 1.1325 year-to-date low.

GBP/USD fell below its 21-day moving average of 1.3359 and remained biased lower amid dollar haven demand and a bearish pattern of lower highs and lower lows. USD/JPY surged above 163.50, with strong dollar demand, higher yields and geopolitical tensions keeping the bias bullish despite near-overbought conditions around the key 164.00 level. AUD/USD remains vulnerable after breaking below its 10-DMA, with broad USD strength and bearish technical signals suggesting downside risks remain.

Treasury yields were up 1 to 6 basis points as the curve flattened, with the ten-year yield reaching a new 18-mo. high of 4.713%. The 2s-10s curve was down about 1 basis point to +33.7bp.

The S&P 500 fell 1.35% on weakness in consumer and tech shares.

WTI oil surged over 6% to its highest level since June 11.

Gold fell about 2% while copper dropped 2.6% as yields and the dollar advanced.

Heading toward the close: EUR/USD -0.32%, USD/JPY +0.41%, GBP/USD -0.46%, AUD/USD +0.41%, DXY +0.33%, EUR/JPY +0.09%, GBP/JPY -0.05%, AUD/JPY -0.04%.(Editing by Burton Frierson Robert Fullem is a Reuters market analyst. The views expressed are his own)